The Third Store Check

Every CPG pro has done many of these. There’s a new aisle now.

Every CPG pro has done many store checks. Walking the aisle with the sales partner, watching how consumers approach the category, where their eyes land, what they pick up and put back. That practice is how we learn the ways of the aisle.

Then online shopping arrived, and the aisle moved. We had to learn a new game — the black art of SEO, search rankings, paid placement, and the algorithm. It wasn’t a game many of us were trained on, but the decision moment had moved to a search bar and a results page, and the work was the same: be where the consumer is looking, in the form they recognise.

You may not like the game, but you have to know it. That has been true of every shift this industry has been through.

Now there’s a third layer. AI is making actual picks, and agents are doing the checkout. We are watching this in real time, the way we watched e-commerce twenty years ago. The shelf is moving again, and the decision moment with it.

What does this game look like? What is the state of play?

The new aisle

Here is the shape of it. A consumer opens ChatGPT and asks for Greek yogurt recommendations under five dollars for a friend who is lactose intolerant. The model returns three names with a short reason for each. Or she asks Perplexity for the best laundry detergent for a household with allergies, and gets back a ranked list with citations from Reddit threads and product reviews. Or she tells Amazon’s Rufus to buy the trail-running shoes that just got reviewed in that podcast she heard, and an order goes through without her ever opening a results page.

Fifty million shopping queries a day on ChatGPT alone, according to recent estimates. Adobe measured a 47x year-over-year jump in generative AI traffic to US retail sites between July 2024 and July 2025. Walmart launched its Sparky agent inside ChatGPT in March. Amazon’s Rufus is running at roughly a twelve-billion-dollar annualised run rate. Google rolled out the Universal Commerce Protocol at NRF — Visa, Mastercard, Target, Walmart, Wayfair, Best Buy, and Home Depot all signed on in the first wave.

The infrastructure is being built faster than we are paying attention. The aisle has a different shape now. The decision moment is happening inside a conversation, not in front of an end cap or with a friend or family member.

Did you know who’s winning it?

Last week, 5W Public Relations released the first ranking of American grocers by how often they get cited in AI-generated answers. The methodology was unglamorous:

Eighty consumer-intent queries across a dozen sub-categories — best overall, cheapest, best private label, best organic, best meal planning, best delivery, best regional

run across ChatGPT, Claude, Perplexity, and Google AI Overviews

scored on citation frequency, position in the answer, sentiment, and sub-category dominance

The result is the new league table.

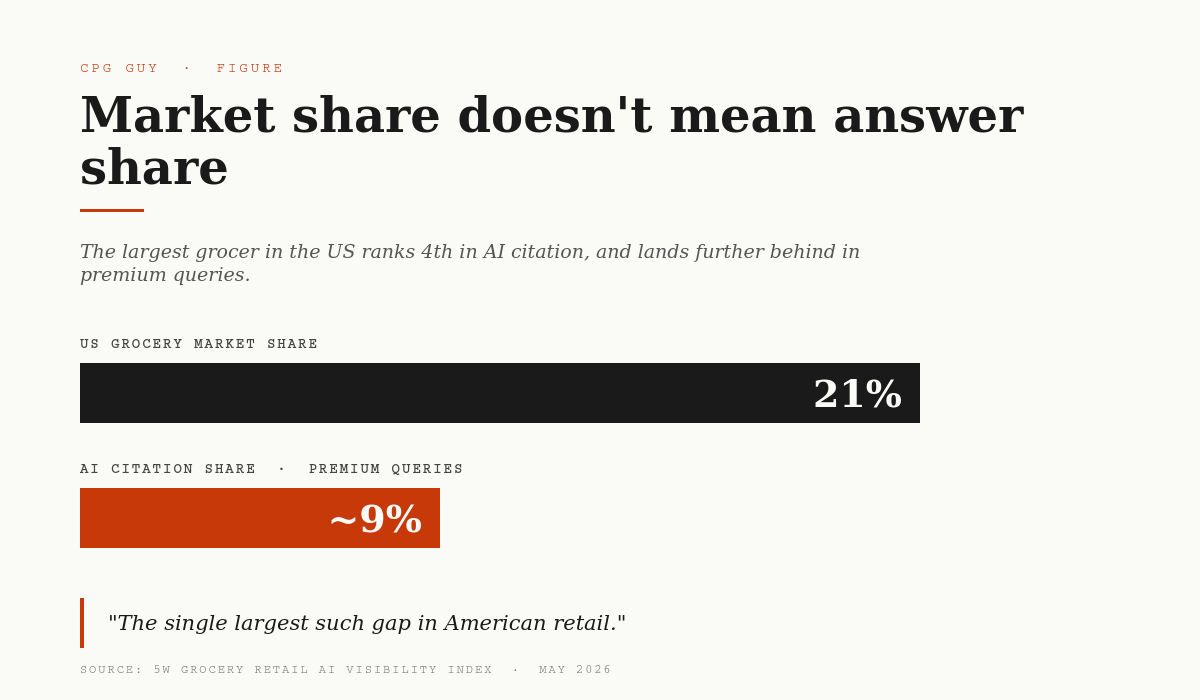

The top ten, in order: Costco, Trader Joe’s, Whole Foods, Walmart, Kroger, Aldi, H-E-B, Publix, Wegmans, Target.

Walmart, with roughly 21% of the US grocery market share, ranks 4th in AI citation share and lands at an estimated 8-10% in premium queries. The single largest such gap in American retail, by 5W’s count. Regional chains punch three times above their physical footprint in their home markets. Reddit and TikTok turn out to be load-bearing: Perplexity pulls a majority of its answers from community sources, and ChatGPT and Claude weigh Reddit heavily.

And here is the line that should have our attention:

“Market share is a lagging indicator. AI citation share is a leading indicator.“— Ronn Torossian, Founder, 5W Public Relations, May 7, 2026

The grocers who close that gap in 2026, he says, will define the category in 2030.

The receipt

Here is where most of us expect the next sentence to be: Indicated Action - optimise for AI.

There are now acronyms: GEO, AEO, LLMO, AI Visibility — and a garden industry of vendors and consultants selling each one. But that read is upside-down: AI is not a new shelf we optimise for. It is a receipt for the shelves we already built — or didn’t.

Look at how the citation actually gets made. Large language models do not rank based on paid placements or backlinks. They surface what comes up most consistently in their training data:

Mention frequency

Co-occurrence — how often the brand name appears alongside the category

Position — first cited or footnoted

Sentiment — recommendation or warning

The Reddit thread where someone wrote four paragraphs about why their Kirkland paper towels held up better than the national brand is worth more to the model than a hundred banner ads.

This is exactly what brand equity is, captured in a story instead of a survey.

Kirkland did not optimise for the AI shelf — Kirkland built two decades of consumers asking for Kirkland by name, in reviews, in recipes, in forums, in “what I bought at Costco” videos. The AI is now indexing that. Same with Trader Joe’s. Two-Buck Chuck, the cookie butter, the everything bagel seasoning — the corpus has been writing about Trader Joe’s for years. The model is doing what models do, distilling and multiplying what was already there.

What we are reading on the shelf

This changes a few things about how we read the new aisle.

The category captain conversation just changed. A private label that has compounded into a destination brand is now a private label with an AI distribution arm. On the Q2 2026 earnings call, Costco’s Ron Vachris named one piece of the strategy plainly:

“Leaning in on Kirkland Signature where we have the most control of the supply chain.”— Ron Vachris, CEO, Costco

Twenty years of consumers writing “I get this at Costco” is now the source material the AI is summarizing back to the next shopper. Costco’s private label is now a media asset.

The national brands are starting to act on it. In February, Unilever signed a five-year deal with Google Cloud explicitly to reorganise around AI-mediated discovery. The quote came not from the CMO but from the Chief Supply Chain and Operations Officer, Willem Uijen:

“As brands are increasingly discovered and chosen in environments shaped by AI, we must lead this shift.“— Willem Uijen, Chief Supply Chain & Operations Officer, Unilever

When the supply chain leader is on the record about brand discovery, the shift is no longer a marketing problem but an enterprise problem. Unilever is treating it that way.

In terms of the optimization playbook, the vendors selling AEO (and the rest) are correct that visibility matters, just that they are upside-down about how it is earned. You cannot buy your way into being the answer consumers already give — you have to have earned it. The mention frequency is the input, and the brand work is the “AI work”. They are the same game, running through a new layer.

If we do not see that, we will solve the wrong problem well.

The store check never ended. The aisle just got another layer.

We walked the first one in the morning, with the sales partner, watching the consumer. We learned to walk the second one through a search bar, playing catch-up with the algorithm regularly, whether we liked it or not. The third aisle is being built right now, out of everything that came before — every mention, review, conversation that put our brand in people’s homes.

The work has not changed. The aisle has. We have done this before.

Further Reading:

5W Public Relations, U.S. Grocery Retail AI Visibility Index 2026, May 7, 2026

Costco Q2 2026 earnings call commentary, via Store Brands, March 2026

Unilever-Google Cloud partnership announcement, via Marketing Dive, February 17, 2026

Walmart Sparky inside ChatGPT launch, via Retail Dive, March 25, 2026

Amazon Q4 2025 earnings disclosure on Rufus, via PYMNTS

Agentic commerce protocol and infrastructure overview, via Rye, March 2026

Agentic commerce state of play, via eco.com, 2026

AI visibility and LLM citation mechanism, via Yotpo, March 2026

Walmart-OpenAI partnership announcement, October 14, 2025